Managed Trade: The Case of Beef in U.S.-China Trade

Huan Zhu from the Herbert A. Stiefel Center for Trade Policy Studies at the Cato Institute, explores the impact of the US-China Phase One Deal on beef, considering the effect of managed trade on a competitive market.

Shares of beef in a Guangzhou supermarket in 2018. Image (c) Huan Zhu 2020

Last month, the United States and China signed an “Economic and Trade Agreement.” One noteworthy feature of the Agreement is that it has a chapter on “Expanding Trade.” Unfortunately, this chapter is different from what we usually see in trade agreements. Instead of liberalizing trade, the chapter has specific commitments for China to purchase U.S. goods. “Expanding Trade” is really just a nice polite way of saying “managed trade.” This “managing trade” approach is wrong. It puts the Agreement and bilateral trade relations in an unstable position and sets a bad precedent.

What’s in the deal?

In the “Expanding Trade” Chapter, China promised to buy $200 billion worth of additional goods (including agricultural goods, energy and services) over the next two years, on top of the trade value of U.S. exports to China in 2017. For agriculture, Article 6.2 says:

“For the category of agricultural goods identified in Annex 6.1, no less than $12.5 billion above the corresponding 2017 baseline amount is purchased and imported into China from the United States in calendar year 2020, and no less than $19.5 billion above the corresponding 2017 baseline amount is purchased and imported into China from the United States in calendar year 2021.”

How such number breaks among different agricultural products is not disclosed to the public. But a former Trump administration official has stated that the expected purchase for beef is US$1.5 billion.

There are many questions about this number: How would China implement it? Will China’s economy support such purchase, as the coronavirus has hit the economy hard? Can U.S. producers increase their production to meet the sales targets? How would other nations respond? There are no answers at this moment.

The history of beef trade

Back in 2000, China used to import a lot of U.S. beef. While the overall demand for beef was small (only USD$16 million in 1998), U.S. beef took up to 44 percent of market share. The ratio grew to almost three-quarters in 2003. However, after a BSE scare, China started banning U.S. beef.

In 2017, the 100-Day Action Plan reached between the Trump administration and Chinese officials lifted the ban. At the time, U.S. officials touted such deal and suggested it would greatly increase beef exports to China.

Unfortunately, the trade war between the two nations began soon after. Most U.S. beef products, along with many other goods, faced between 10 percent and 35 percent additional tariffs imposed by the Chinese government, as responses to the Trump administration’s tariffs of up to 25 percent on $360 billion Chinese goods. Even though China recently announced that it would reduce retaliatory tariffs by half on $75 billion worth of U.S. goods, beef products are still subject to 5 percent to 30 percent tariffs.

As a result, even with the removal of the ban in 2017, U.S. beef only witnessed an incremental increase to China. As shown in Table 1 below, U.S. beef exports increased from almost negligible to USD$63 million in 2018. The number is only a small fraction of the rapid growth of the overall beef market in China, from USD$2.6 billion to 4.9 billion during the same period. The imports from other major beef-exporting countries, including Argentina, Australia, Brazil, New Zealand, and Uruguay, all witnessed a much larger jump than U.S. beef. The only exception is Canada, which faced a beef ban for four months, which was lifted in 2019.

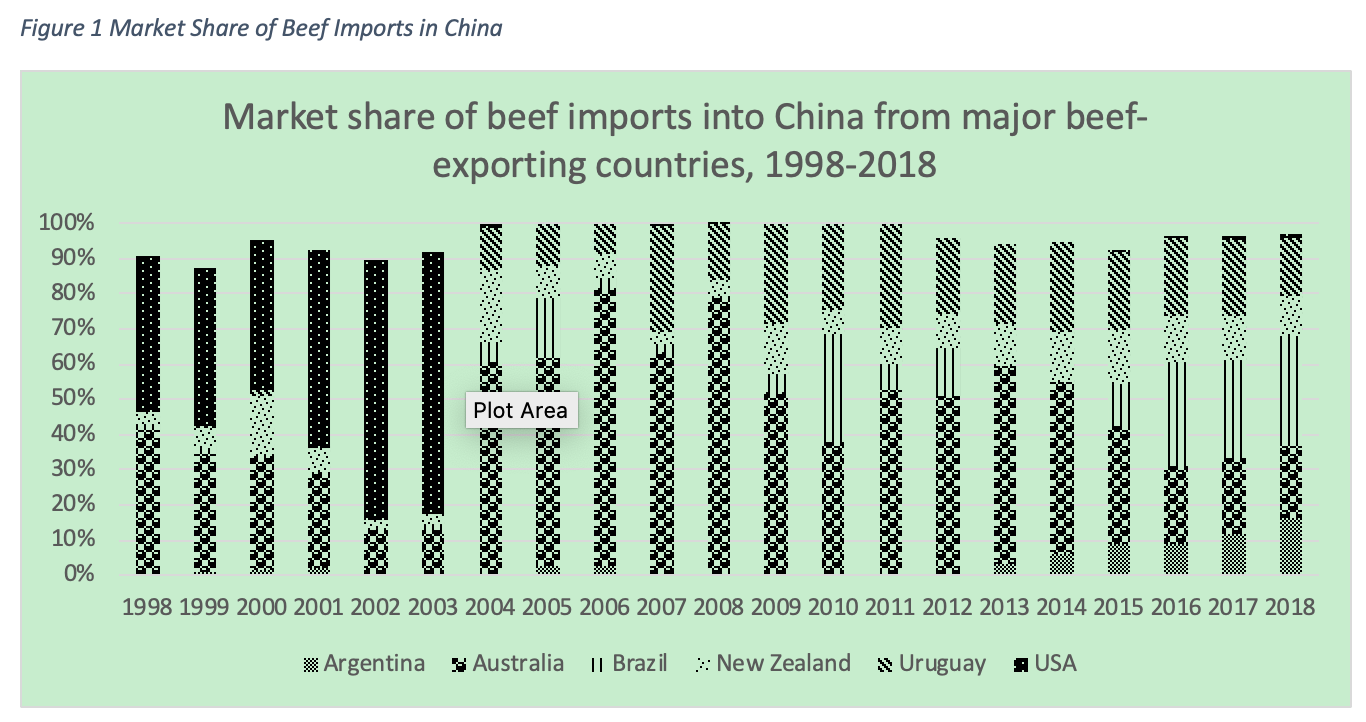

In terms of market share (see Figure 1), U.S. beef now takes up 1.3 percent of the beef market in China. It is up from 0.03 percent in 2016, but the share is still much less than the 75 percent market share the U.S. used to enjoyed back. Other major beef producing nations, such as Argentina, Australia, Brazil, New Zealand and Uruguay, seem to maintain dominance in the Chinese market, as the market rapidly expands.

It is possible for the United States to export additional 1.5 billion beef exports to China over the next two years, considering China’s beef market grew $2.3 billion in the past two years. But that means U.S. beef will have to compete with beef products from other major beef-exporting countries. Does U.S. beef have a competitive advantage?

Obstacles remain

In fact, U.S. beef faces some competitive disadvantages compared to its competitors.

For a start, even though China rolled back its additional tariffs on beef, U.S. beef still faces up to 30 percent retaliatory tariffs in China. This is on top of the ordinary 12 percent to 25 percent of tariffs American beef already faces. In comparison, Australian beef currently faces a 4.8 percent to 17.5 percent tariff rate, as a result of the China-Australia FTA. That tariff will be phased out sometime between 2019 and 2024 (depending on the product in question). New Zealand exporters already face zero tariffs because of the China-New Zealand FTA. That means U.S. beef will be more expensive than many other beef products in China’s market.

Non-tariff barriers may also curb U.S. beef exports. The good news is, the Agreement addresses most of them. For instance, China commits to relax its strict bans on synthetic hormones that are commonly used by U.S. ranchers. China also agrees to relax its traceability standards. In addition, China now allows older U.S. cattle to be exported. These measures will, in theory, help boost U.S. beef into China.

However, in reality, Chinese consumers may already be used to hormone-free beef from Australia and Brazil. Their fears of synthetic hormones, science-based or not, may deter them from buying U.S. beef. In order to succeed in the Chinese market, the U.S. exporters need to learn more about the preference and needs of Chinese consumers. It is not mission-impossible, but certainly takes more effort and time.

The impact of managed trade

It is laudable that the Trump administration was able to remove some Chinese non-tariff barriers for its products. However, its move towards managed trade, setting up specific purchase goals, does more harm than good.

First, it puts the Agreement and bilateral trade relations in an unstable position. If China fails to import the promised amount of beef from the United States, then what? According to the “Dispute Resolution” chapter, the United States could start a consultation process. If consultations do not resolve the issue, the United States may impose unilateral remedial measures. China, if it disagrees with such remedial measures, is barred from taking countermeasures or challenging it. Instead, it may only withdraw from the Agreement. It is possible that China’s failure to meet all the purchase goals could lead to a total breakdown of the Agreement. And then we will see a replay of the tariff war and economic decoupling that we have been thought over the past two years.

Second, it sets a bad example for all future trade agreements. The United States may be able to twist the arms of countries that are more dependent on the U.S. economy than the other way around. That may serve the U.S. interest the best at the moment. But what if we start seeing other bigger countries twisting medium size countries’ arms, and medium size economies’ twisting small countries’ arms? Who will be there to protect small countries from being bullied?

By Huan Zhu, Research Associate, Herbert A. Stiefel Center for Trade Policy Studies, Cato Institute (Washington, D.C.).